Why AI Is Changing Software, Not Destroying It

The enterprise software panic narrative is everywhere.

Public software valuations, especially for SaaS companies, have come under significant pressure, driven by what observers have described as “AI anxiety.”

That pressure has been compounded by high valuations and uncertainty around the returns from heavy AI spending.

Coding agents like Claude Code, OpenAI’s Codex, and Cursor have lowered the technical barriers to building software. AI agents and orchestration tools are extending the potential for automation. As enterprises evaluate whether they can build what they used to buy, they are actively rationalizing vendor sprawl, consolidating tools, and demanding clearer returns on every line of their IT budgets.

Yet the reality is far more complex. AI is not destroying enterprise software. SaaS is not collapsing.

Instead, a structural advancement is underway. The real story is a deepening bifurcation in the software market that is creating very different outcomes for companies depending on how software is built, delivered, and monetized.

At Revaia, we believe this is a moment that rewards rigor over reflex. Rather than reacting to sentiment, we have taken a data-driven, product-level, and operations-level approach to understanding how AI is reshaping enterprise software. We analyzed public market performance against qualitative criteria like workflow embeddedness, switching costs, and operational criticality.

What follows is a summary of that analysis and the investment framework it has revealed. We’re sharing some of these insights in the hope they offer a valuable lens to others trying to understand the impact of AI on software at this pivotal moment.

A Bifurcation in Software

To make sense of the noise, Revaia went back to first principles and built what we called a “Software Bifurcation Index.”

From there, we analyzed public software companies through that lens, drawing on earnings calls, product disclosures, and market commentary to assess how exposed or advantaged each category might be as AI adoption accelerates.

This is essentially a way to separate signal from sentiment in public markets. Rather than starting from stock performance and working backward, the team flipped the approach. We began by defining a set of product and technology criteria that we believe matter most in the AI era, rooted in the principles that underpin our day-to-day investment decisions in private markets. This includes factors such as how deeply a product is embedded in customer workflows, the complexity of its integrations, the nature and defensibility of its data, and whether it delivers measurable, mission-critical outcomes.

From there, we analyzed public software companies through that lens, drawing on earnings calls, product disclosures, and market commentary to assess how exposed or advantaged each category might be as AI adoption accelerates.

What emerged was a clear split, or as we dubbed it: a bifurcation.

On one side are the Structurally Advantaged. These are companies whose products are deeply integrated, data-rich, and difficult to displace, often benefiting from strong customer dependence, regulatory complexity, or roles that are infrastructure-like within the enterprise. This includes platforms that power critical operational workflows, manage proprietary data, and support essential business infrastructure, such as cybersecurity, ERP, and observability tools.

On the other side are the Structurally Exposed. These products are easier to replicate because they are lighter-weight tools, often built around features rather than workflows, with less proprietary data and fewer barriers to switching. These are the categories where AI is already compressing differentiation. New tools can replicate functionality faster and more cheaply, and enterprises are consolidating their vendor lists as budgets tighten. The additional squeeze comes from platform giants such as Microsoft, Salesforce, and Google, which are absorbing point-solution functionality into their own AI copilot offerings.

The point isn’t that one group wins and the other disappears. But the market is already beginning to distinguish between foundational and optional software.

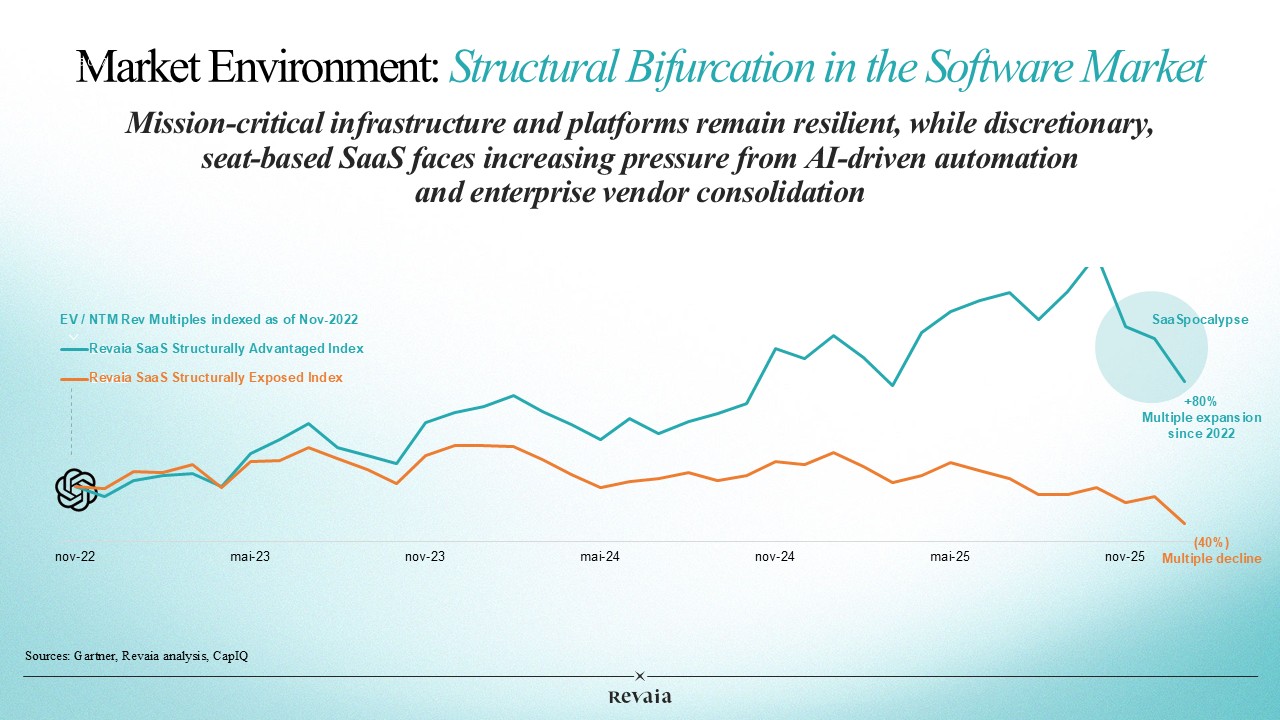

This bifurcation is not theoretical. Analysis of public software companies reveals an approximately 120% valuation gap between the two groups since the emergence of generative AI in November 2022. Companies positioned on the mission-critical side of the divide have seen their valuation multiples expand by roughly 80%, while those on the discretionary, seat-based side have experienced declines of around 40%. The key dividing line comes down to switching costs: the companies being amplified are architecturally embedded in their customers’ operations, while the displaced can be removed without rearchitecting anything.

Why Enterprise Software Remains Structurally Durable

To understand this transition, it helps to clarify a common misconception. SaaS is not a sector. It is a delivery-and-monetization model. Software has historically evolved through distinct phases: from on-premise perpetual licenses, to cloud-based subscriptions, and now toward AI-native and agentic architectures. The current disruption is not primarily about whether software matters. It is about how its evolving value proposition gets monetized.

Historically, SaaS relied on multi-year contracts, seat-based Annual Contract Value (ACV) scaling, and usage-based pricing. AI is shifting that dynamic. Software is increasingly shifting toward usage-based and dynamic pricing models, including token-based, task-based, and outcome-based pricing. In a context where AI agents perform tasks autonomously, revenue can scale independently of headcount. Instead of paying for access to a tool, customers increasingly pay for what that tool accomplishes.

The SaaS commercial model may evolve, but the underlying importance of software to every business remains unchanged.

Context, Trust, and Scale

Despite the rapid progress of AI, enterprise software platforms retain several fundamental advantages that explain why established systems are likely to remain central to business operations:

- Context: Enterprise software providers hold sovereignty over proprietary customer data and deeply embedded workflow intelligence developed over years of business integration. Large language models do not naturally possess this firm-specific operational knowledge, which gives incumbents a meaningful edge.

Speaking at Revaia’s recent AGM, Edouard de Mézerac, CEO of AI consultancy Artefact, argued that the data layer is becoming the most defensible dimension of any software business because foundation models have exhausted what public data can offer. What is happening now, he explained, is "a data hunt. All these AI models are chasing private data to improve their models, and many companies are realizing that they have a really strong data patrimony that they have never looked at in this way."

Deepki, a Revaia portfolio company that helps the real estate industry transition toward sustainability using data and AI, also demonstrates the context advantage.

The company manages data on tens of thousands of buildings across more than 90 countries, building a proprietary data layer that no general-purpose AI model could replicate. As founder and CEO Vincent Bryant explained, this accumulated, curated data about individual data represents a powerful advantage: "If you want to help the business make important decisions, you must be able to build insights that are based on good data, reliable data, comprehensive data, relevant data," he said.

- Trust: Enterprise environments call for robust governance that includes audit trails, permissions, compliance systems, and accountability. Agentic AI must operate deterministically within enterprise guardrails. In regulated industries such as banking, healthcare, and insurance, even small error rates can pose unacceptable operational risk. 99% accuracy is equivalent to 100% wrong.

What ultimately matters is a vendor’s ability to demonstrate a strong track record in real-world deployments, deep domain expertise, and a clear sense of accountability. Questions of data sovereignty, long-term reliability, and strategic vision often outweigh purely technological considerations.

That’s the case with Intersec. The company helps telecom operators and governments analyze mobile metadata, including real-time geolocation data from approximately one billion connected devices. Intersec's public safety deployments include national alert systems used in conflict zones and during natural disasters. Such services demand a proven track record that no amount of rapid coding can replace, according to founder and CEO Yann Chevalier.

"When you put your trust into a vendor to help you make sense of that data, you need to feel in a relationship of trust,” he said. “You need to feel that your data is going to be safe. And this is not so much correlated to AI itself. It's much more correlated with who the vendor is in front of you…If tomorrow there was a new entrant who would be able to replicate some large pieces of our software using AI, I don't think they would have a good play if they don't have the right answers to these security and sovereignty questions."

- Scale: Enterprise platforms operate on existing infrastructure, such as systems of record and systems of action already integrated into core business processes. This embedded footprint enables vendors to scale AI adoption productively across large installed customer bases, rather than starting from scratch.

Frontify, which provides brand management software to some 1,300 companies worldwide, demonstrates how an embedded platform can scale AI capabilities across a large installed base.

Founder and CEO Roger Dudler described the company's strategy as pushing functionality down toward the infrastructure layer by building APIs and developer-friendly architecture that connects to customers' existing ecosystems. With relationships spanning over a decade, Frontify's embedded footprint enables it to layer new AI-powered capabilities on top of existing deployments rather than asking customers to start from scratch.

"It's about investing in the infrastructure layer so that it's not a choice for the customers to go somewhere else," he said. Roger also noted a practical reality that cuts against the disruption narrative: [As an enterprise company,] "If you pay 100K, 200K, 300K for a piece of software, it's still cheap. You won't just move that to some vibe coding. That's not going to happen anytime soon." With relationships spanning over a decade, Frontify's embedded footprint enables it to layer new AI-powered capabilities on top of existing deployments rather than asking customers to start from scratch.

Together, these factors represent structural moats that enable incumbent software providers to preserve competitive advantages even as AI reshapes the landscape around them.

Those advantages are compounded by other factors, such as switch costs, which remain one of the most underappreciated sources of defensibility in software. Replacing a deeply embedded system often requires migrating large volumes of data, rebuilding integrations with adjacent platforms, retraining users across the organization, and absorbing the operational risk of disruption.

In mission-critical and vertical contexts where software is woven into regulatory compliance, daily workflows, and industry-specific processes, those costs are especially steep.

When customers are passionate about a product because it delivers measurable ROI, the combination of operational dependency and user loyalty creates a compounding advantage that is extremely difficult for competitors—or AI-native newcomers—to dislodge.

The Next Software Cycle

The AI transition is not simply a story of disruption. It is giving rise to several powerful structural themes that will define the next generation of software winners:

- Cybersecurity and digital sovereignty remain among the most resilient areas of technology spending. Gartner forecasts global information security spend reaching $240 billion in 2026, growing at over 12% year-on-year. Regulatory frameworks like the EU’s NIS2 directive and DORA are expanding the perimeter of mandatory cyber resilience, while sovereign cloud strategies are moving from aspiration to procurement requirement. Gartner expects more than 50% of multinational organizations to have digital sovereignty strategies by 2029.

- Mission-critical infrastructure is being propelled by a multi-year AI compute buildout. Gartner expects data center systems spending to exceed $650 billion in 2026, with server spending alone growing nearly 37% year-on-year. The demand for resilient, always-on platforms will intensify as digitization deepens across energy, healthcare, transport, and public administration.

- Agentic AI and applied AI use cases are moving from experimentation to enterprise deployment. Gartner predicts that 40% of enterprise applications will include task-specific AI agents by the end of 2026, up from less than 5% in 2025, a massive upgrade cycle. But not every experiment will survive: Gartner also warns that more than 40% of agentic AI projects may be scrapped by 2027 due to cost overshoot and unclear outcomes. The durable winners will be those providing measurable value with strong governance.

- Vertical software platforms continue to gain momentum as enterprises seek industry-specific solutions that package domain workflows, compliance requirements, and composable capabilities into tightly integrated stacks. Gartner expects broad enterprise adoption of industry cloud platforms by 2027, supporting verticalized systems of record that are especially defensible against horizontal disruption.

The European Opportunity

The AI transition also creates a distinct opportunity for Europe. Tech investment is on track for approximately €44 billion, with 2024 marking a clear bottom and valuations more disciplined than in 2021. Europe’s tech ecosystem now represents roughly 15% of GDP, up from around 4% in 2016, according to Atomico’s 2025 State of European Tech. That growth reflects a structurally larger, more mature foundation for building category leaders.

This backdrop is strengthening. In 2025, 36% of European VC investment flowed into deep tech, up from 19% in 2021. The European Investment Bank’s “Tech EU” plan targets €70 billion between 2025 and 2027, intending to catalyze approximately €250 billion in private capital across AI and digital infrastructure.

While Europe’s regulatory environment is often cited as a drag on growth, it can be used by European companies to their advantage. In a world where compliance, data governance, and sovereignty are critical for enterprise adoption, companies that can navigate complex, multi-jurisdictional markets build the kind of moats that are hard to replicate.

At the same time, rising focus on digital sovereignty and support for scale-ups, such as the proposed EU Inc. framework, signals a shift in how Europe values its tech champions.

For investors with deep European expertise and operating capability, this convergence of disciplined valuations, ecosystem maturity, and institutional tailwinds creates an unusually attractive window.

The Next Era of Software

The SaaSpocalypse makes for captivating headlines, but misses the real story. Software is not disappearing. It is evolving.

The model is changing, competition is intensifying, and the market is bifurcating between platforms deeply embedded in enterprise operations and tools that sit on the surface.

For investors, this is less a crisis than a reset. Winners will be mission-critical, hard to replace, capital-efficient, and built to integrate AI. Demand remains strong: IT spending and the AI transformation cycle is still early.

This isn’t the end of software. It’s a more selective era, favoring the embedded over the replaceable and the efficient over the cash burning.

For those with the right lens, the opportunity is significant.