Unlocking the Future of Climate Tech: Inside Revaia’s Climate Deep Dive Workshop

Earlier this month in Paris, Revaia hosted an intimate roundtable on the future of climate tech as part of the Unlock VC conference for women venture capitalists. The gathering brought together European leading female investors.

The session, held at Revaia’s Paris offices, was designed as a workshop, a space for reflection and collective intelligence. As firm believers in the long-term potential of climate innovation, we saw this as a way to signal our commitment to the ecosystem, share insights, and listen to how other investors are preparing for the next generation of this critical sector.

Because this was a private event, we can’t reveal the names of attendees or the direct conversations. But we do want to share some of the key takeaways and themes.

Overall, a spirit of collaboration defined the tone of the afternoon. The group was clearlyenergized by the opportunity to strengthen the foundations for a new phase of growth.

Shifting Market Landscape

Climate tech is an industry best characterized by both sobering realities and compelling opportunities. Over the past 18 months, capital flows into climate tech have slowed dramatically. Fundraising remains difficult both for startups and funds, as risk appetite softens and late-stage financing dries up.

After years of exuberance, the uncomfortable truth is that even promising companies are struggling to survive as late-stage financing has become increasingly scarce.

Political and regulatory uncertainty adds another layer of complexity. From the climate-skeptical rhetoric emerging in U.S. politics to evolving European Union climate regulations, volatility has become a defining feature of the market.

Yet amid this turbulence, participants noted a growing commitment from generalist funds to integrate sustainability into their theses, whether by launching dedicated climate verticals or embedding ESG dimensions across their portfolios. This trend suggests that despite headwinds, climate tech is becoming mainstream rather than remaining a niche concern—a development that bodes well for the sector's long-term capital access.

Tomorrow's Climate Tech Winners

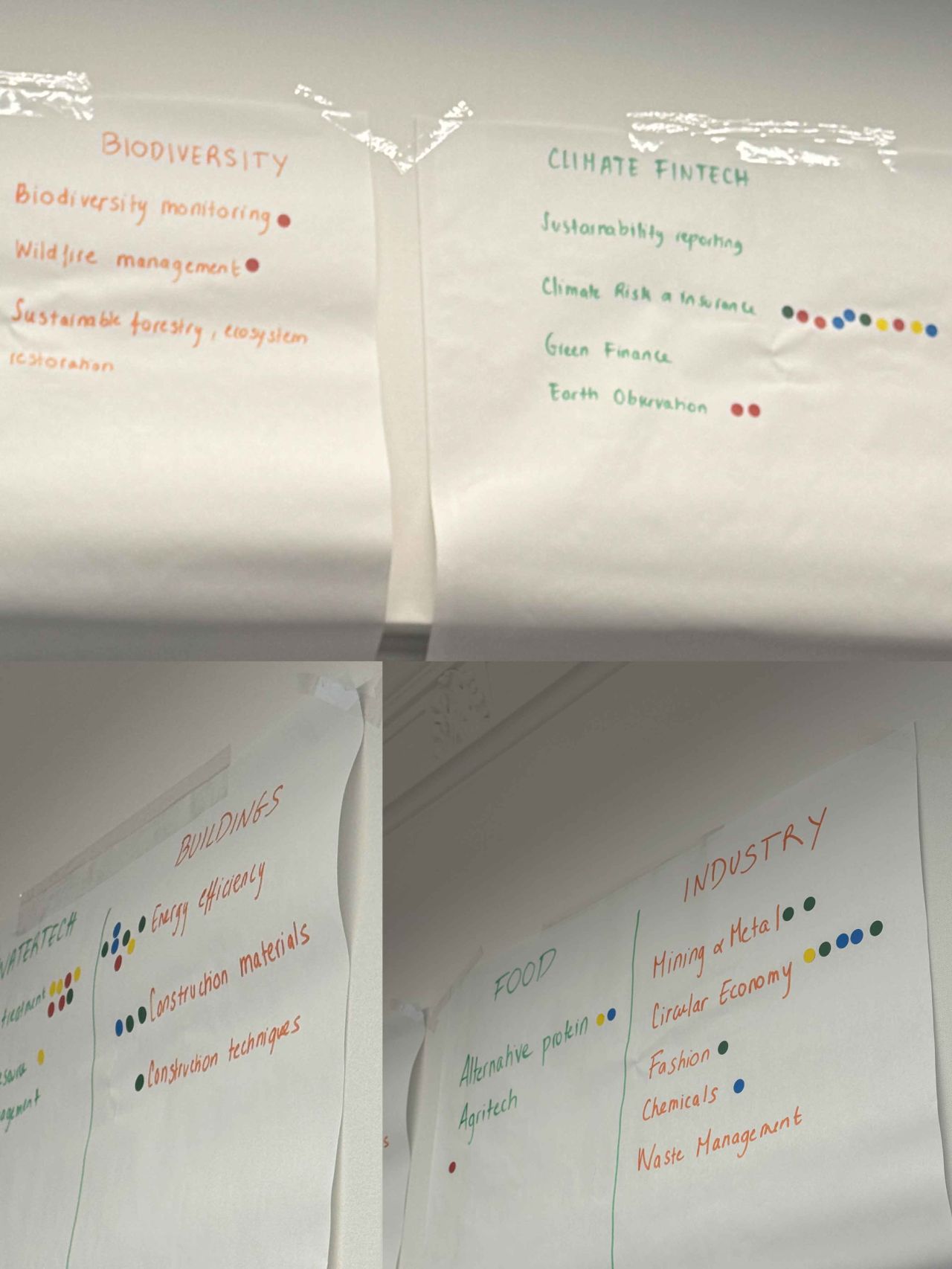

As part of the workshop, attendees voted on which climate verticals they expect to gain traction over the next 12–24 months. The exercise revealed a collective recalibration: a pivot from headline-grabbing moonshots toward infrastructure, resilience, and efficiency.

Five sectors dominated the discussion:

- Grid Technologies – Modernizing and stabilizing power infrastructure emerged as a top priority. With electrification accelerating across industries, grid resilience is becoming a critical enabler for the energy transition.

- Energy Efficiency – Investors see renewed potential in software-driven solutions that optimize consumption and reduce costs, particularly in industrial and real estate sectors.

- Water Treatment – Wastewater innovation, long underfunded, is gaining attention as droughts and contamination crises highlight the link between water management and climate adaptation.

- Circular Economy – Material reuse and recycling technologies are maturing, with opportunities for scalable business models that go beyond consumer waste.

- Climate Risk and Insurance – From flood prediction to wildfire protection, climate risk modeling remains early-stage but increasingly essential for managing systemic climate exposure.

ClimateTech Deep Dive workshop — identifying priority innovation themes across sectors.

While enthusiasm for nuclear fusion and advanced nuclear persists, participants see these as decade-long plays rather than short-term opportunities. Conversely, biodiversity, once a hot topic, has cooled due to difficulties in quantifying returns. Similarly, AgriTech continues to face scalability and unit economics challenges.

This pragmatic tone reflects a broader industry shift: from visionary idealism to operational realism. The next frontier in climate tech isn’t just about invention. It’s about implementation.

The conversation also revealed telling insights about sectors that have lost their luster:

- Biodiversity, which enjoyed significant momentum just a year ago, now faces investor fatigue due to challenges in achieving financial scalability.

- AgriTech, despite its critical importance to climate mitigation, continues to struggle with persistent scalability and unit economics challenges that make it a difficult investment proposition for many funds.

Nuclear technologies presented an interesting case study in long-term thinking. Both fusion and advanced nuclear solutions were viewed as compelling but distant opportunities, with investors projecting a 10-year horizon for meaningful commercialization. Notably, waste storage was once considered the primary obstacle. That no longer dominates concerns, suggesting progress in addressing this historical challenge.

Adaptation vs. Mitigation

One of the more animated exchanges of the afternoon centered on the tension between adaptation and mitigation. The divergent interpretations among investors revealed fundamental differences in investment philosophy and impact measurement.

Many impact-driven funds continue to focus on mitigation: reducing emissions through technologies like carbon capture or renewable energy. Adaptation, by contrast, remains harder to quantify and less compatible with traditional VC models.

This highlights a critical gap in the climate tech ecosystem. While mitigation technologies offer clearer metrics and often more scalable business models, the growing reality of climate impacts makes adaptation increasingly urgent.

The challenge for the venture community will be developing frameworks that can adequately capture the value of adaptation investments. That reinforced a core theme of the day: the need for creativity not just in technology, but in finance itself.

The Dual-Use Debate

Few topics sparked as much debate as dual-use innovation: the overlap between climate technologies and defense applications.

Earth observation satellites originally developed for environmental monitoring are now being deployed for security and defense. The maritime industry offers a similar example: underwater sensing technologies designed for ocean conservation are being repurposed for naval surveillance.

Several funds expressed discomfort with the potential militarization of climate technologies, while others argued for a more pragmatic approach that recognizes the reality of multiple revenue streams and scaling pathways.

The convergence between climate and defense reflects both the dual nature of the technologies and the increasing role of data in securing strategic assets. The challenge for investors is to navigate this intersection thoughtfully while balancing societal impact with market opportunity.

While opinions diverged, the discussion captured a deeper truth: innovation rarely fits neatly into silos. In an interconnected world, climate technology will increasingly cut across domains, from energy and materials to infrastructure and geopolitics.

Standards, Scalability, and Segment Maturity

Beyond the thematic debates, several operational challenges emerged as consistent pain points. Certification remains a major bottleneck. Startups developing new materials or industrial processes often struggle to navigate fragmented and slow-moving standards, delaying adoption.

Segment maturity also varies widely. Electric vehicles and mobility are consolidating, sustainability reporting has slowed following the EU’s Corporate Sustainability Reporting Directive (CSRD) rollout, and while battery storage continues to attract investment, questions linger about total addressable market and recycling economics.

This regulatory friction represents both a barrier and an opportunity for investors willing to navigate complex approval pathways.

From Reflection to Strategy

Despite the candid recognition of market challenges, climate tech remains a generational opportunity, though one that demands sharper execution, stronger collaboration, and deeper patience.

The sector’s cooling cycle may, paradoxically, be its best moment for recalibration. As speculative capital retreats, the focus shifts back to fundamentals: measurable impact, sustainable economics, and enduring innovation.

Because if there’s one thing all participants at the workshop agreed on, it’s that the climate story is far from over. The crisis of climate change continues and the most important chapters for innovation are just beginning. The need to address decarbonization and growing climate impacts is only growing more urgent.

Ambition anchored in realism may well define the next chapter of climate investing. The downturn, rather than deterring Revaia, has reinforced our belief that long-term value creation lies in solving humanity’s hardest problems.

Success will come to those investors who can navigate current market conditions while maintaining focus on the transformative potential of climate technologies.

For Revaia, this convergence of pressure and possibility underscores that this is a moment for clarity and conviction. What will distinguish the next generation of climate tech investors is the ability to discern what’s real, scalable, and durable in climate innovation.

Rather than dampening spirits, these challenges call for sharpening our focus on identifying the most resilient climate tech opportunities.